New to budgeting and on Baby Step 1? We’re so glad you’re here! This guide will help you start your first monthly budget.

Right now, you’re trading the short-term rush of immediate gratification for the peace of financial success over the long term. And that’s hard work. So, keep in mind that budgeting on Baby Step 1 means squeezing every last penny out of each budget category—clipping coupons, eating rice and beans, and selling so much stuff the kids think they’re next!

I know you can do this. Your future self will be so thankful you did!

The Best Way to Budget

Before you actually start budgeting, let’s talk about what we’re aiming for: a zero-based budget.

A zero-based budget doesn’t mean you have zero dollars in your bank account—it means you’ve subtracted all your monthly expenses from your monthly income until the amount left is zero. You’ve given every dollar a job to do!

Your zero-based budget is your plan for the month. It’s not just a way to track spending your money on whatever you want. So, if you keep going way over or you’re not making progress on your money goals, you really need to buckle down and stick to what you decided you could afford before the month began.

You can create a zero-based budget the old-fashioned way with a sheet of paper, or you can use our super easy and free budgeting app, EveryDollar, inside Ramsey+.

Let’s Find Your Money

When it’s time to start your budget (we’ll get there in the next section), these are the numbers you’ll need:

1. Your Monthly Income

Add up all the money you bring in and put this total at the top of your budget. This includes paychecks, side hustles, residual income, child support and any other cash you expect to bring in. If it’s money that comes into your household’s bank account, it’s income!

2. Your Monthly Expenses

You need to include every expense you’ll have for the month. Most expenses will fit into the categories I recommend in this guide, but feel free to come up with your own too!

The best thing to do is to look at your last couple of bank statements and make sure you’ve included everything.

3. Your Seasonal Expenses

Pull out your calendar as you work through this part. What expenses do you have coming up that you can start planning for now? Christmas is in December every year, so it doesn’t exactly sneak up on you. Birthdays, anniversaries and car tag renewals shouldn’t surprise your budget either.

For example, if you’re going to spend, say, $500 on Christmas, you’ll need to start budgeting about $40 per month in January. If you start saving in June, that number jumps to about $70 per month.

4. Your Cushion

You’re aiming for zero dollars left in your budget, but it would make anyone nervous to have zero dollars in their bank account at the end of the month. Most people leave an extra cushion—anywhere from $100–300—in their checking account that isn’t counted in their income. When you start this process, budget for that cushion and then try to forget it’s there.

So, your first month would have a line under the Saving category labeled Cushion. You only budget for it once, and every month after, it just provides a small, invisible buffer in your checking account.

Budgeting Isn’t One-Size-Fits-All

Now that you know the numbers you need to create a zero-based budget, let’s apply what you’ve learned to your unique situation.

![]()

Start budgeting with EveryDollar today!

The median household income in America is $61,937.1 And just like that number doesn’t tell everyone’s story, there’s no one-size-fits-all budget either. This guide is based on averages. Everyone’s budget will look a little bit different based on a number of factors—like where you live, if you have kids, how far you commute to work and more.

Don’t feel bad if you need to adjust your numbers frequently as you get started. It takes people about three months to get the hang of budgeting. So, give yourself some grace and stick with it! Before you know it, you’ll be in control of your money, telling every dollar where to go, and well on your way to a $1,000 emergency fund!

It’s time to get out your numbers and start your own monthly budget! Ready? Let’s do this!

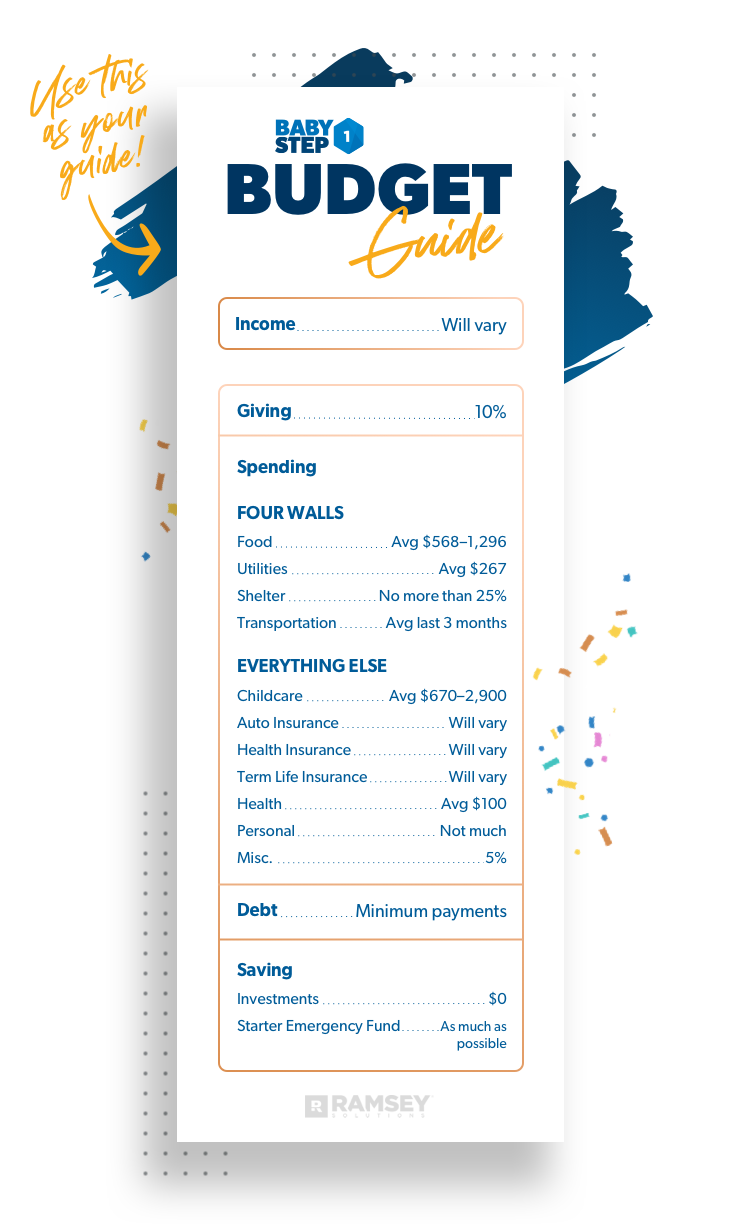

The Budget Guide

Income

Will Vary

Your income should include paychecks, small-business income, side hustles, child support and any other cash you bring in. If it’s money and comes into your household’s bank account, it’s income!

Put the total at the top of your budget. There you go—that’s all the money you have to work with this month. Then it’s time for my favorite part: Let’s tell every dollar where to go!

Giving

10%

When you’re saving up for that $1,000 emergency fund, every dollar counts. So, you may be wondering why I want you to give 10% of your income during this stage. I mean, what’s the point in working your butt off to save money if you’re just going to turn around and give it away?

Hear me out on this: In all my years of living and breathing personal finance, I know that people don’t experience true financial peace until they become generous givers. Why is that? Because giving changes you.

The reason I teach people to start giving immediately, even when they’re in Baby Step 1, is because financial health isn’t just about the math—it’s about your heart too.

Giving is the mechanism that moves you from selfish to selfless.

Even if you don’t have a lot to give right now, you’re setting yourself up to give more in the future. Establishing this habit will not only impact the lives of others, but it will also change your heart.

But most people forget to make giving a priority in their budget. If you wait until the end of the month to give from whatever’s left, you probably won’t have much to give. That’s why you should prioritize giving above everything else, no matter what Baby Step you’re on.

Give it a try. When you make your budget, assign 10% of your income to giving. As a believer, I give this money to my local church. Where you give is totally up to you and your family—just make sure your giving follows your personal values.

Giving is the most fun you’ll ever have with money. It’s addictive—in the best way possible. So, go out and give a little until you can give a lot. I promise you that it will be worth it.

Spending

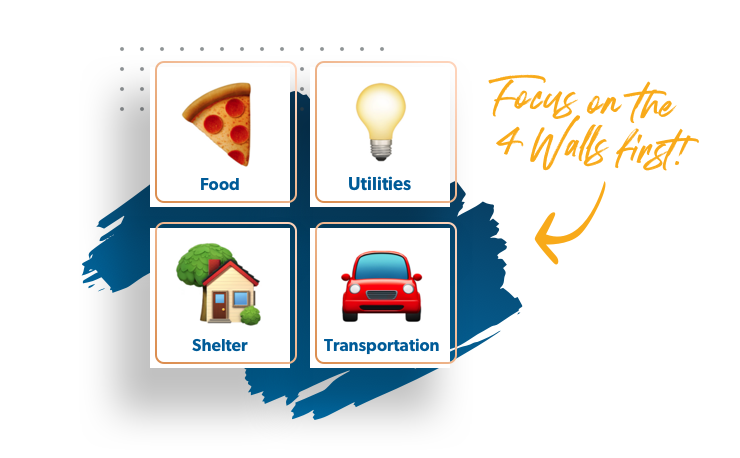

The Four Walls

Your family comes first. Make sure your priorities are in order and start by taking care of your necessities first. Don’t get behind on your utility bills just to stay current on your Mastercard or student loan payments.

If you’re going to be behind on something—and I’m not recommending being behind—choose to pause paying, or pay less, on your unsecured debt.

Credit cards and student loans are examples of unsecured debt—that means the lender can’t take anything away from you (like a car or a house). Unsecured debt is typically going to be the last debt you pay if you’re in trouble. The first debt you pay should be something they can take, so make sure you focus on the Four Walls first:

- Food

- Utilities

- Shelter

- Transportation

1. Food

Will vary: The average American family of four spends between $568–1,296 a month.2

This number only includes groceries and meals prepared at home, and it’s an average. But you don’t want to be average! Try to spend even less so you can put extra money in your starter emergency fund.

Eating out at restaurants goes in another category you’ll see later (the Personal Spending/Recreation category) while you’re on Baby Step 1, because on this Baby Step, you shouldn’t see the inside of a restaurant unless you’re working in it!

6 Ways to Lower Your Grocery Bill

- Meal plan. The reason this helps save money is because you know exactly what you need to buy to feed your family all week, without relying on last-minute takeout or impulse purchases at the store. Plus, when you get strategic about what to make, you can cook a big batch or use the same ingredients in multiple recipes.

- Make a grocery list. This will help you stick to your budget, avoid buying impulse items, and remember everything in just one trip.

- Take out cash for groceries. Let’s say you’ve budgeted $600 for groceries every month. When you get paid, take that $600 in cash out of the bank. Then, when you go to the grocery store, you use that cash to pay for the groceries. Having cash for a budget category like groceries is great because you always know exactly how much you have left to spend in each category each month.

- Try discount grocery stores like Aldi. Smart shopping isn’t only about what you buy, but where you buy. We all know certain stores are more expensive than others, so be mindful of that. I’ve heard of people saving up to half of their grocery budget simply by making the switch to Aldi!

- Shop generic. This is a super simple hack to save about one-third of your money without even cutting back! Making the switch from name brand to generic on things like pet food, shampoo, coffee, medicine and more will make you feel like you got a raise.

- Use coupons. When it comes to grocery shopping on a budget, it would be crazy not to include coupons. It’s basically free money! And coupons aren’t only in the Sunday paper anymore. Use Google to search for the product you need and type the word coupon after it. Just remember the trick with coupons: They only save you money if you were going to buy the product anyway.

2. Utilities

Will vary: The average American family of four spends $267 a month.3

This number includes electricity, natural gas, water and garbage/recycling. Your location can have a big effect on how much you spend in this category. For example, if you live in Florida, your utility bills will cost more in the summer than someone who lives in Washington and isn’t blasting the air conditioning!

In this Baby Step, your utilities do not include cable, high-speed internet, Netflix or unlimited cell phone data. These are lifestyle expenses, not essentials. So, for now, I encourage you to cancel these subscriptions.

Remember, right now you’re cutting back on everything. Once you’re in a better position financially, you can have Netflix back!

3. Shelter

No More Than 25% of Your Take-Home Pay

Here’s what’s included in the 25%:

- Rent or mortgage payment

- Renter’s or homeowner’s insurance

- Private mortgage insurance (PMI)

- Homeowners association (HOA) fees

- Property taxes

Making sure this total is at or below 25% will keep you from buying more house than you can afford. But what happens if you’re already spending way more than 25% on your housing expenses? It may be time to downsize.

If you’re struggling to keep up with your mortgage, consider selling your house and moving into something more realistic for your budget. You can also try lowering your monthly payment by connecting with Churchill Mortgage to see your refinancing options.

4. Transportation

Will Vary

To get your average, look at how much you’ve spent on gas over the last three months. That’s your amount to budget for gas each month. Or if you live in a big city and use public transportation, this is where you budget for your fare.

Don’t forget to budget for transportation-related expenses that come up every few months, like oil changes and preventative maintenance.

As you work through this Baby Step (and the next two), it’s important to limit your transportation expenses. This isn’t the time to take a road trip with your friends. It is the time to find the best deals on gas and transportation that you possibly can! Live like no one else, so later you can live and give like no one else.

We just wrapped up your Four Walls! In the rare case you run out of money before this part of your budget is done, you may have an income problem. The good news about life is that it’s not a snapshot—it’s a filmstrip. You’re not stuck where you are right now.

If that’s you, make a change! That means rethinking your job and maybe your career. In the meantime, pick up a part-time job, because you’ve got to get your income up.

Now that you’ve got the essentials covered, let’s move on to . . .

Everything Else

Childcare (if Applicable)

Will vary: The average American family spends between $670–2900 a month.4

This category will cover childcare expenses that are necessary for you to go to work. We aren’t talking about paying the neighbor girl so you can have a date night—going out for fun is on pause during this Baby Step.

Childcare costs vary a lot based on what state you live in, what type of childcare you go with, and how many children you have. It’s a personal decision, and we have some tips on how to budget for it here.

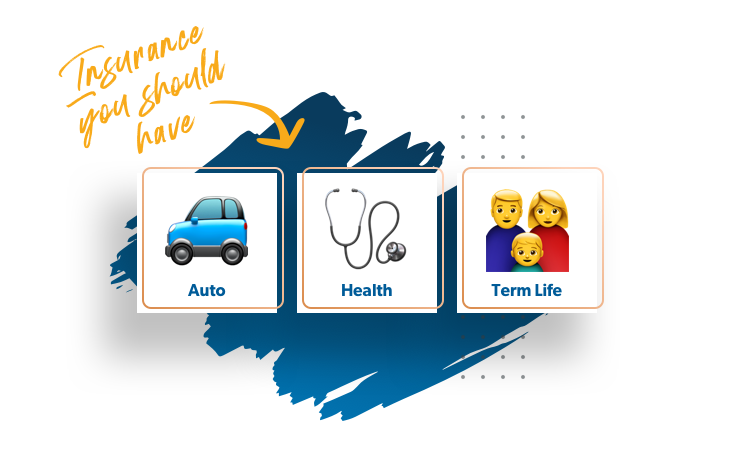

Insurance

You still need to be properly insured in Baby Step 1—and throughout all the Baby Steps. When you’re looking for things to cut out of your budget, this is not the place. But there are some things you can do to save money on insurance.

Let’s talk about three types of insurance you need:

- Auto insurance

- Health insurance

- Term life insurance

Auto Insurance

Will Vary

This cost will depend on what type of car you own, how much coverage you need, where you live and many other factors. My advice is to always shop current rates once a year—especially if you’ve had a ticket or an accident on your record. Those things aren’t held against you forever, so if you’ve been a safe driver for a while, your rates should lower.

Health Insurance

Will Vary

Health insurance costs will depend on how much coverage you need, what your employer does or doesn’t offer, how often you visit the doctor, and many other factors. My advice is to shop current rates, look into Health Savings Accounts (HSAs) for tax savings, and think about increasing your deductible to bring down monthly premiums.

Term Life Insurance

Will Vary

I know it isn’t fun to think about life insurance, but it needs to be a priority. If you were to pass away unexpectedly, how would your spouse pay for monthly expenses without your income? In a time like that, the last thing anyone should worry about is making ends meet.

So, how much coverage should you get? A 15- to 20-year term life policy that covers 10 to 12 times your annual income is what you need to take care of your loved ones—and it’s actually really affordable. Most people can get term life insurance for the cost of a Netflix subscription (or less)!

And even stay-at-home parents need life insurance. There’s no one-size-fits-all because every family is different, but a 15- to 20-year policy between $250,000–400,000 is a general rule. You need to think through what you’ll do in three major areas: childcare, education and household duties (if the stay-at-home parent were to pass away). Those decisions might mean you get a bigger policy to cover any extra costs.

So, those are the types of insurance you can’t afford to go without. But there are some types of insurance you don’t need. If someone tries to sell you accidental death insurance, mortgage protection insurance, supplemental insurance for medical issues, or whole life insurance . . . run!

To see every different type of insurance we recommend, take our Coverage Checkup to make sure you’re covered—or to save some money on your current rates.

Health

Will vary: The average American family spends about $100 per month.5

Unfortunately, health insurance isn’t the only expense related to your health. This category includes, but isn’t limited to:

- Medications

- Co-pays

- Supplements

- First aid supplies

Personal Spending/Recreation

Not much!

In Baby Step 1, you’re putting every extra dollar into your emergency fund. Restaurants, movies, new clothes and unnecessary things should be avoided right now. But I know it’s not realistic to say you can’t have any fun—that’s how people fall off the wagon. Just be sure to think through your purchases carefully and try to keep them to a minimum. You’ve got so much more to gain by not spending right now!

Miscellaneous

5% of Your Take-Home Pay

The reality is, you probably won’t get some of your expenses exactly right, especially if you’re new to budgeting. If you need to replace a lightbulb or forget that your kid has a field trip this month, this category will keep you covered. And if you don’t spend everything in your Miscellaneous category, that’s great! Move it over to Savings to give that a little boost!

Debt

Only Your Minimum Payments

You aren’t paying anything extra on debt in Baby Step 1. That’s because, just for this step, you’re focusing on building up a $1,000 starter emergency fund. Any extra money you can find will go there!

Ever heard of Murphy’s Law? Murphy’s Law says anything that can go wrong will go wrong. The Baby Steps will help you get everything in order so you can get out of debt and build wealth, but first, you need to protect yourself against Murphy.

Unexpected things happen in life—your car tire goes flat, your dishwasher breaks, you chip a tooth. This starter emergency fund will put a buffer between you and those events. When you’re deep in debt, an emergency fund will turn a crisis into an inconvenience. Let that peace of mind keep you motivated as you sacrifice and save in Baby Step 1!

Saving

Investments

$0

You shouldn’t be putting money into your retirement accounts right now. Your money should be going toward your emergency fund, so turn off your investing. Yep, even if it’s matched by your employer. (If you already have money in your retirement accounts, leave it there. But pause on investing new money for now.) Trust me, I want you to be investing in your future! But right now, giving yourself the safety net of an emergency fund is the best investment you can make. You’ll get to invest in your retirement later on in Baby Steps 4 and beyond!

Starter Emergency Fund

As Much as Possible With Gazelle Intensity

On Baby Step 1, you’re trying to save a $1,000 starter emergency fund as fast as you can!

Depending on how much experience you have saving money, you could be in and out of this step in no time—or it could feel impossible.

That’s why you need gazelle intensity. Dave Ramsey coined the term after reading Proverbs 6:4–5 (NKJV), “Give no sleep to your eyes, nor slumber to your eyelids. Deliver yourself like a gazelle from the hand of the hunter, and like a bird from the hand of the fowler.”

In other words, when you’re in over your head with money problems, you need to work as hard as a gazelle works to run from a cheetah. You need that kind of serious, “run like your life depends on it” action. That, you guys, is gazelle intensity. Save like your life depends on it!

5 Ways to Save $1,000 in One Month

- Cut back your spending. When we polled our Facebook followers, their number one savings tip was to avoid eating out at restaurants. What else could you cut out? Think about how much you could save if you cut out cable, manicures, unlimited cell phone data, Starbucks or Amazon Prime.

- Sell some stuff. Right now, having savings should be more important than having stuff—so sell some stuff! Put that vinyl you haven’t listened to in years up on Craigslist or Facebook Marketplace. Host a garage sale and sell those “antiques” collecting dust in your basement. Clean out your closet and make some money on Poshmark.

- Increase your income. Picking up a part-time job or working overtime might not be what your friends are doing, but “normal” is broke—and you’re tired of being broke! So, for this season, pick up extra hours to build up extra savings.

- Gather up all your loose change and cash. Go find the $10 Aunt Susie put in your birthday card that you stuffed in a drawer somewhere or dig all those quarters and dimes out of your center console. It may not add up to $1,000, but it will help you get started.

- Check your tax deductions. Do you get a big tax refund every year? A lot of people think this is free money, but actually, it was your money to begin with—and the government has been borrowing it interest-free! You can put that money back into your paycheck every month by adjusting your tax withholding.

Don’t Give Up!

It takes about three months of budgeting to get into the groove. So, don’t give up if it’s messy at first. It’s okay to keep adjusting your categories until your budget works.

If you create a budget by following these guidelines, you won’t be wondering where all your money went at the end of the month. You’ll actually be able to save up that starter emergency fund even faster and gain real momentum throughout the rest of the Baby Steps! Stick with it and don’t forget: A budget doesn’t limit your freedom—it gives you freedom.

Read the full article here